Which is better: saving or investing?

Find out whether saving or investing is better for you, based on your goals. Learn how to combine both habits to achieve long-term financial stability and growth

PERSONAL FINANCES

Iván Morales

4/12/20254 min read

Introduction

Talking about money means making decisions. One of the most common—and also most important—is this: What’s better to do with my money: save it or invest it? While both options may seem similar, they actually serve very different purposes. Understanding their differences and when to apply each is key to making smarter financial decisions.

In this article, we’ll explore the value of saving, the purpose of investing, and how to find the right balance between the two to achieve greater financial peace of mind.

The Value of Saving

Saving, simply put, means setting aside part of the money we earn to use later. It might sound obvious, but not everyone does it—or does it consistently. Often, saving gets postponed because we think we can’t afford it, or because we prefer to spend in the present without thinking much about the future.

However, saving plays a very important role: it gives us security. It’s the cushion that protects us during emergencies, unexpected events, or life changes like illness, job loss, or home repairs. It also allows us to plan in advance for desired events like a vacation, back-to-school expenses, or even a big purchase.

Having savings—even a small amount—helps reduce financial stress. It gives us a sense of control and allows us to make decisions more calmly.

What About Investing?

Investing, on the other hand, means putting that saved money to work with the goal of growing it over time. Unlike savings, which usually stays untouched and unchanged, investing involves taking some level of risk. However, it also offers the opportunity for greater rewards.

When we invest, our money can grow through interest, returns, dividends, and more. This allows us to reach bigger goals in the medium or long term, such as buying a house, starting a business, or planning for a more comfortable retirement.

Investing is not the same as gambling, and it’s not just for experts or people with lots of money. Today, there are accessible options like investment funds, interest-bearing savings accounts, or even digital tools that let you start with small amounts.

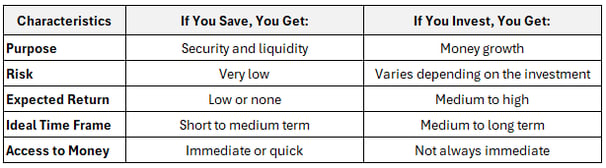

Key Differences

Let’s take a look at some of the key differences between saving and investing:

Both actions are important, and you don’t necessarily have to choose just one. In fact, the key lies in combining them strategically.

Why isn't saving alone enough?

Many people believe that saving is enough. However, over time, inflation—the general rise in prices—causes saved money to lose value.

For example, if you save $1,000 today, in five years that same amount will likely not buy as much as it does now. Money loses purchasing power, even if you don’t spend it.

That’s where investing becomes essential. Investing not only helps preserve the value of your money—it helps it grow over time. It’s like planting a seed: if you take care of it and give it time, it will bear fruit.

When is saving the better option?

Saving is ideal when:

You’re building an emergency fund.

You’re planning a major expense in the near future (within a year).

You want to avoid going into debt.

You have irregular income and need financial stability.

You prefer to keep your money accessible in case of emergencies.

It’s recommended to save at least three to six months’ worth of your basic monthly expenses in an easily accessible fund. This gives you peace of mind to handle unexpected situations.

When is it time to invest?

Once you’ve built an emergency savings cushion and your basic finances are in order, it’s a good time to start investing.

Some signs that you might be ready to invest include:

You want your money to grow over time.

You’re willing to let your money “work” for several years.

You have medium- to long-term goals.

You’re learning about investment options and understand there are risks involved.

You don’t need a lot of money to start investing. What matters most is starting with what you have and continuing to learn as you go.

So, which is better?

The answer is: it depends on your situation and your goals.

Saving is the first step. It lets you sleep well at night, knowing you have a safety net.

Investing is the next step. It helps you achieve your long-term goals and dreams.

They’re not opposites—they’re allies with different purposes. What matters is learning how to use both wisely and in balance.

A practical example

Imagine you receive some extra income. Instead of spending it all or saving it all, you could divide it like this:

50% to savings (for emergencies or short-term expenses)

30% to medium- or long-term investments

20% for enjoyment (something you want or need right now)

This kind of distribution lets you make progress on different fronts—security, growth, and enjoyment—all at once.

Conclusion

Saving and investing aren’t opposing paths—they’re complementary.

Saving protects your present; investing prepares you for the future.

Good financial health comes from knowing when to do what, based on your goals, possibilities, and level of understanding.

The most important thing is to make informed decisions and stick to your habits. With discipline, time, and small consistent steps, you can build a healthier, more stable, and prosperous relationship with money.

If you want to keep learning, I invite you to check out my full review of the Personal Finance: How to Manage Your Money Successfully ebook.

I hope you find it helpful!

Contact

Sign up for the latest updates

© 2025 - Industrias SAIKDI S. A de C. V. - Todos los derechos reservados